Article by

Paul Pontenagel

For most of the past two decades, US electricity demand was flat, with efficiency gains offsetting population growth, manufacturing declining. The grid enjoyed a long period of relative stability, which meant that grid operators planned around slow, predictable change.

However, over the last few years, artificial intelligence has been steadily driving a wave of data center construction across the United States at a scale and speed that the grid was not designed to absorb. The facilities powering AI model training and inference can draw more than 100 MW of power continuously, enough to supply around 80,000 American homes, and the largest campuses now under development are multiples of that.

The power markets responsible for keeping the lights on are already responding. Wholesale electricity prices are rising in the regions absorbing the most new load, capacity markets are tightening, interconnection queues are backlogged, and the generation mix capable of actually serving this demand is not being built fast enough to keep pace.

This article looks at where the pressure is hitting hardest, what it is doing to price signals and market structure, and what it means for participants active in or considering entry into US wholesale power markets.

If this is your first time reading about USA’s wholesale power markets, we recommend you start with how the USA’s wholesale power markets function before continuing this article.

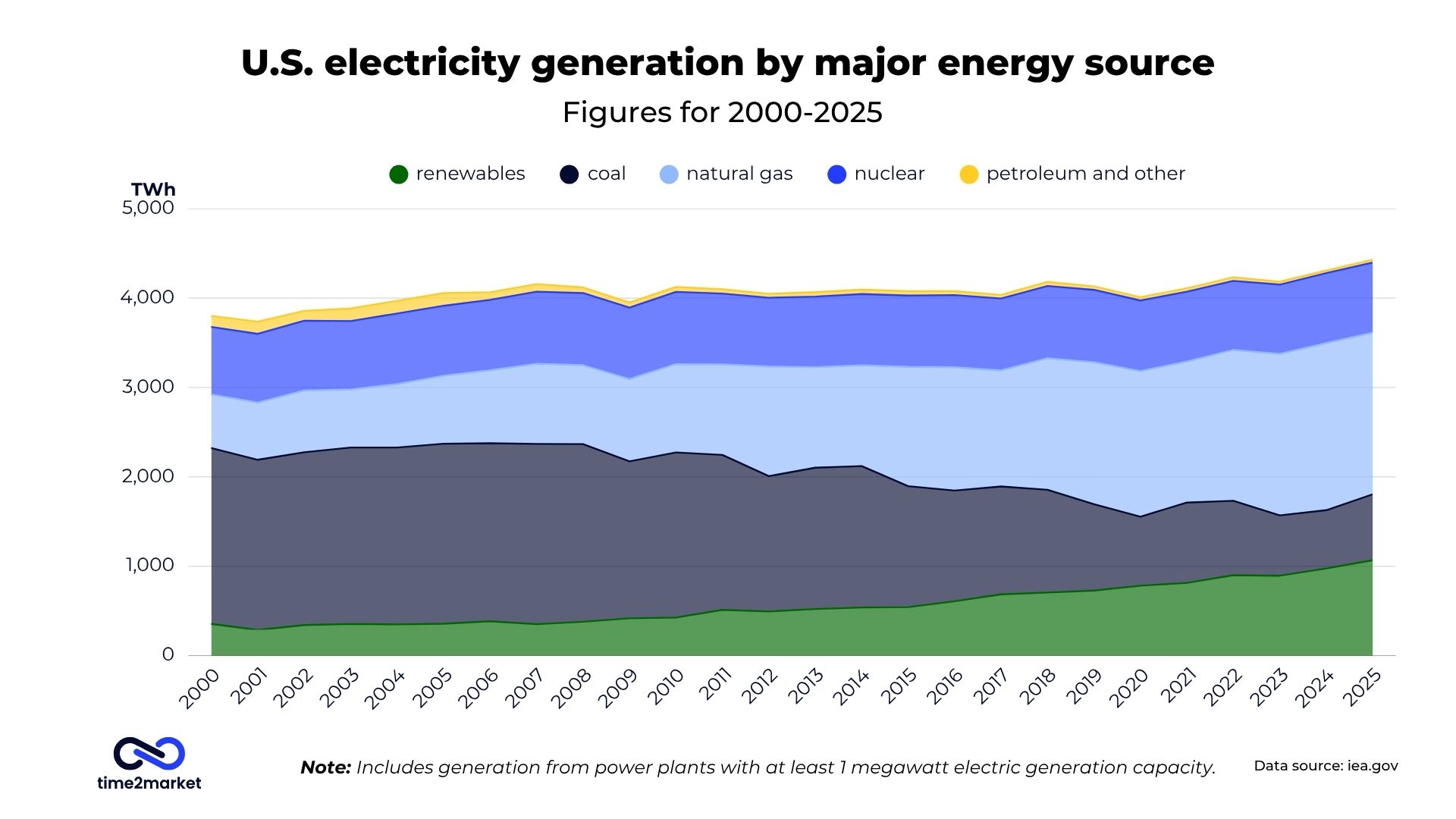

Electricity demand in the United States is entering its first sustained growth period in roughly two decades. The US Department of Energy projects total energy demand could grow by 15 to 20% over the next ten years, a reversal driven by the convergence of electrification, onshoring of manufacturing, and, most significantly, data center expansion. Data centers are not the only factor, but they are the fastest-growing and the hardest for grid operators to plan around.

US data centers consumed approximately 176 TWh of electricity in 2023, around 4.4% of total national consumption. The Electric Power Research Institute puts data centers at up to 9% of US electricity generation by 2030. Goldman Sachs has projected US data center power demand rising from 31 gigawatts in 2025 to 66 gigawatts by 2027.

To put that in physical terms: a single hyperscale data center consumes as much power as roughly 80,000 American homes. If all data centers currently permitted in the US come online, their combined electricity use would exceed the total annual consumption of every US state except Texas.

The IEA projects that global data center electricity consumption will double by 2030, with AI-focused facilities tripling their power use over the same period.

The volume of demand is only part of the challenge. The more pressing issue for power markets is the nature of the demand that data centers put on the grid.

Data centers require continuous power 24 hours a day, seven days a week, regardless of weather, season, or time of day. Unlike residential or commercial demand, which follows predictable daily and seasonal patterns, data center load does not taper at night or ease in mild weather. For grid operators accustomed to forecasting demand curves, a large new baseload customer that operates at near-constant draw is a fundamentally different situation.

The speed of deployment compounds this. A hyperscale data center can be planned, permitted, and operational within two to three years. New transmission lines, substations, and generating capacity typically take five to ten years or longer to bring online. The result is a growing mismatch between where new demand is landing and where the grid has capacity to serve it.

Geographic concentration adds a third dimension. Data centers do not distribute themselves evenly across the grid. They cluster near fiber networks, in low-tax jurisdictions, and close to existing power infrastructure, creating sudden, large load pockets in specific regions and at specific nodes.

Finally, AI workloads introduce a demand profile that grid operators are still learning to manage. AI inference and training tasks create rapid, large swings in power draw, which can strain the technical capabilities of both grid-connected and on-site generation sources.

Data center growth is not evenly distributed across the United States. Developers cluster where land is cheap, fiber infrastructure exists, tax incentives are generous, and existing power capacity is available. The result is that a small number of regions are absorbing a disproportionate share of new demand and their grid operators and power markets are responding accordingly.

The most acute concentration of data center demand in the United States is in Northern Virginia, particularly Loudoun County, which has earned the name "Data Center Alley." The region hosts the world's largest concentration of data centers by any measure, and new development continues. The PJM Interconnection, which operates the grid serving 67 million people across 13 states, as well as Washington DC, is absorbing more new large-load interconnection requests than any other ISO in the country.

As a result, capacity market dynamics in PJM have changed significantly. As new large loads enter the queue faster than new generation clears, capacity auction prices have risen sharply, with implications for both physical market participants and financial positions tied to capacity.

Texas is the second major pressure point for data center demand. ERCOT, which operates as an isolated grid outside the broader US interconnected system and is not subject to FERC jurisdiction in the same way other ISOs are, has seen rapid data center build-out across the state, with particular concentration in the Houston corridor, the Permian Basin, and the Dallas-Fort Worth area. The load growth in ERCOT over recent years has been among the fastest of any ISO in the country, driven by a combination of AI datacenters, cryptocurrency mining operations, and industrial electrification.

ERCOT's market structure with its energy-only design, real-time pricing, and lack of a traditional capacity market means that the impact of large new loads manifests differently than in PJM. As data center load adds a persistent, weather-independent floor to demand, the dynamics of ERCOT's real-time market are shifting in ways that are not yet fully understood.

ERCOT is also in the process of implementing its Real-Time Co-optimization with Batteries program, which will change how ancillary services and storage resources are dispatched in real-time. The interaction between this market redesign and the incoming wave of large new loads adds an additional layer of complexity for market participants.

Beyond PJM and ERCOT, data center growth is beginning to reshape market dynamics across other ISO regions, though the developments are not as demanding for now. MISO, which covers a large portion of the Midwest and parts of the South, is seeing new large-load interconnection requests in areas that had little industrial load growth for years. SPP, which covers the central plains, is similarly receiving data center and cryptocurrency mining interconnection applications in regions where transmission infrastructure was not built with this type of load in mind.

In the Western Interconnection, CAISO and the utilities operating outside organized markets are also tracking significant proposed data center development, though build-out in the West has so far been slower than in Virginia or Texas, partly due to water availability constraints and higher land costs in established tech corridors.

Across all regions, a common theme is emerging: interconnection queues have grown faster than the grid's ability to process and connect new projects. The vast majority of projects that enter interconnection queues never reach completion, but the volume of requests alone is creating planning and cost challenges for grid operators that are beginning to feed through into market prices and capacity outcomes.

The demand surge in dense data center areas is already feeding through into the price signals, capacity outcomes, and congestion patterns that define the trading environment in US wholesale power markets. Three dynamics are worth examining in detail.

Capacity markets exist to ensure that enough generation is available to meet peak demand not just today, but in the years ahead. Generators and demand resources bid into forward capacity auctions, and the clearing price signals whether the market expects to be adequately resourced.

In PJM, where the capacity market is most developed and most closely watched, capacity auction prices have risen sharply as the volume of new large-load interconnection requests has outpaced the addition of new dispatchable generation. The 76% increase in PJM wholesale power costs in the first quarter of 2026, documented by their own Monitoring Analytics, is the clearest single data point illustrating how quickly this dynamic is moving.

ERCOT operates without a traditional capacity market, relying instead on an energy-only design where scarcity pricing during tight supply conditions provides the investment signal for new generation. As data center load adds a persistent baseload floor to ERCOT demand, the frequency and magnitude of scarcity pricing events is expected to increase, though the precise timing and scale remain difficult to forecast.

In nodal power markets, prices are set at individual locations on the grid, known as locational marginal prices, or LMP. When transmission constraints prevent power from flowing freely from generators to load, prices diverge between locations. This divergence, known as congestion, is both a cost for physical market participants and a source of opportunity for those trading financial transmission rights and basis positions.

Data center clusters are creating new and intensifying existing congestion patterns in ways that are relevant for anyone active in nodal markets. When a large new load comes online at a specific location, it increases the flow on the transmission paths serving that location. If those paths are already constrained, or if the new load exceeds local generation capacity, congestion increases and LMP spreads widen between the load pocket and the broader hub.

In the regions absorbing the most datacenter growth, particularly in PJM's northern Virginia zone and in parts of ERCOT, congestion costs have risen alongside load growth. New data center clusters effectively create new load pockets, and the transmission infrastructure serving them was not always designed with this volume of demand in mind. For market participants, this means that the congestion landscape in affected regions is introducing volatility to positions that were previously stable.

Every new generator, storage project, or large load that wants to connect to the US grid must go through an interconnection study process managed by the relevant ISO or transmission owner. This process assesses what grid upgrades are needed to accommodate the new connection and allocates the associated resources. In recent years, the volume of interconnection requests has grown dramatically, driven by both renewable energy development and new large loads, including data centers.

The result is queues that stretch years into the future and studies that take longer to complete than the projects themselves take to build. FERC has acknowledged the problem and has introduced reforms through Order 2023, aimed at speeding up the interconnection process. However, the backlog is substantial, and the reforms are still working their way through implementation at individual ISOs.

For data center developers, a congested interconnection queue means that even fully funded, shovel-ready projects face multi-year delays before they can draw power from the grid. This is one of the reasons why on-site power generation, discussed in the next section, is becoming more common.

The demand challenge described in the previous sections has a supply-side counterpart: the US generation mix was not built to serve a new category of large, firm, around-the-clock industrial load at the speed it is arriving. Understanding what can and cannot serve datacenter demand is relevant not just for the developers building these facilities, but for anyone assessing the generation investment signals coming out of affected power markets.

The fundamental requirement for data center power is continuity. Unlike flexible industrial loads that can curtail during tight grid conditions, data centers cannot tolerate interruption. This means that the generation mix serving them must be capable of producing power on demand, regardless of weather conditions or time of day.

This requirement creates a structural problem for a grid that has been adding renewable capacity at scale. Solar and wind are now the cheapest sources of new electricity generation in most US markets, and they dominate the interconnection queue. But they cannot provide firm, dispatchable power on their own. A data center that relies entirely on renewable energy still needs the grid, or on-site backup generation, to cover the hours when the sun is not shining and the wind is not blowing.

Natural gas remains the default solution for many developers. It is dispatchable, relatively fast to build, and available across most US regions, and a significant share of new requests reflect developers pursuing dedicated on-site gas generation rather than relying on grid connections.

Nuclear is also increasingly becoming a part of the conversation. Existing plants offer exactly the profile data centers need and the pipeline of conditional offtake agreements between data center operators and small modular reactor projects grew from 25 GW to 45 GW in under a year, according to the IEA. None are yet operating commercially in the United States, so we’ll have to wait and see.

The delays and uncertainty in the grid interconnection process have pushed a growing number of developers toward on-site power generation. On-site battery storage is becoming a critical technology for managing the characteristic demand swings of data centers, and the IEA notes that with the right market incentives, flexible data centers with storage could ultimately become an asset to grids.

Supply chain constraints are adding a further layer of difficulty. The surge in demand for generation equipment has tightened markets for gas turbines and transformers, contributing to delays even for projects with funding and permits already in place.

The developments of data centers in the USA are reshaping the fundamental dynamics of how these markets price power, allocate capacity, and manage congestion. For participants already active in US wholesale markets, and for those assessing whether and where to enter, several implications are worth drawing out.

Wholesale power prices in the regions absorbing the most data center load are rising while capacity markets in PJM and elsewhere tightening as demand growth outpaces generation additions. Participants with load obligations in affected regions need to be accounting for this in their forward planning.

Congestion patterns are also changing, with new load pockets forming near data center clusters, particularly in PJM's Northern Virginia zone and in parts of ERCOT, widening LMP spreads between those locations and broader hubs. For participants active in nodal markets, this creates both new risks for positions that assumed stable congestion patterns and new opportunities in financial transmission rights and basis trading for those who understand where the grid is tightening.

The regulatory environment further adds a layer of uncertainty that is harder to quantify but equally important. The outcome of the FERC co-location debate, the pace of state-level policy responses, and the still-unresolved question of who pays for grid upgrades will all influence the cost structure and market design of US power markets over the coming years. Participants making long-term market access decisions today are doing so against a heavy regulatory backdrop.

What is clear is that the US power market is in a period of structural transition that is being accelerated by AI infrastructure investment at a scale the grid was not designed to absorb. The markets that emerge on the other side of this transition will look different from the ones that existed before it, more volatile in some regions, more constrained in others, and more complex across the board. For market participants, understanding the mechanics of that transition is the foundation of any credible US power market strategy.

Time2Market helps energy trading organizations navigate the complexity of US wholesale power markets, from initial market entry and market access support to ongoing post-entry continuity. If you are assessing where and how to participate in US power markets, our team of experts is available to help.

Take a look at the markets we can assist you with and get in touch with our team.

Our team of experts has developed an invaluable self-assessment tool based on over 300 successful market entries — so you know exactly where your organization stands before you make your next move.

✅ Takes just 8–10 minutes

✅ Completely free

✅ Receive your tailored report instantly

✅ Trusted by firms managing billions in AUM

Answer 30 questions and receive a personalized readiness report covering your strategic fit, regulatory exposure, financial requirements, and realistic timeline to first trade.

Disclaimer: Time2Market ApS is not responsible for the completeness, accuracy, and actuality of the information provided. This article is intended for informational purposes only and should not be considered business or legal advice. The energy industry is extremely dynamic and counterparties change their requirements frequently. As a result, information discussed on this page is subject to change without notice.

This page has last been updated on

June 11, 2026